As the world steps into an era of clean energy transition and booming high-tech industries, strategic minerals have emerged as the focal point in the geopolitical competition among major powers. If oil was once viewed as the “lifeblood” of the global economy, today critical elements such as gallium, rare earth elements, nickel, cobalt, and tungsten play a decisive role in manufacturing electric vehicle batteries, semiconductor chips, aerospace components, and even medical devices. Any nation capable of controlling the supply or refining chains of these materials gains a powerful strategic advantage in future industries. This explains why the contest over mineral resources has evolved into a struggle for influence on the global stage.

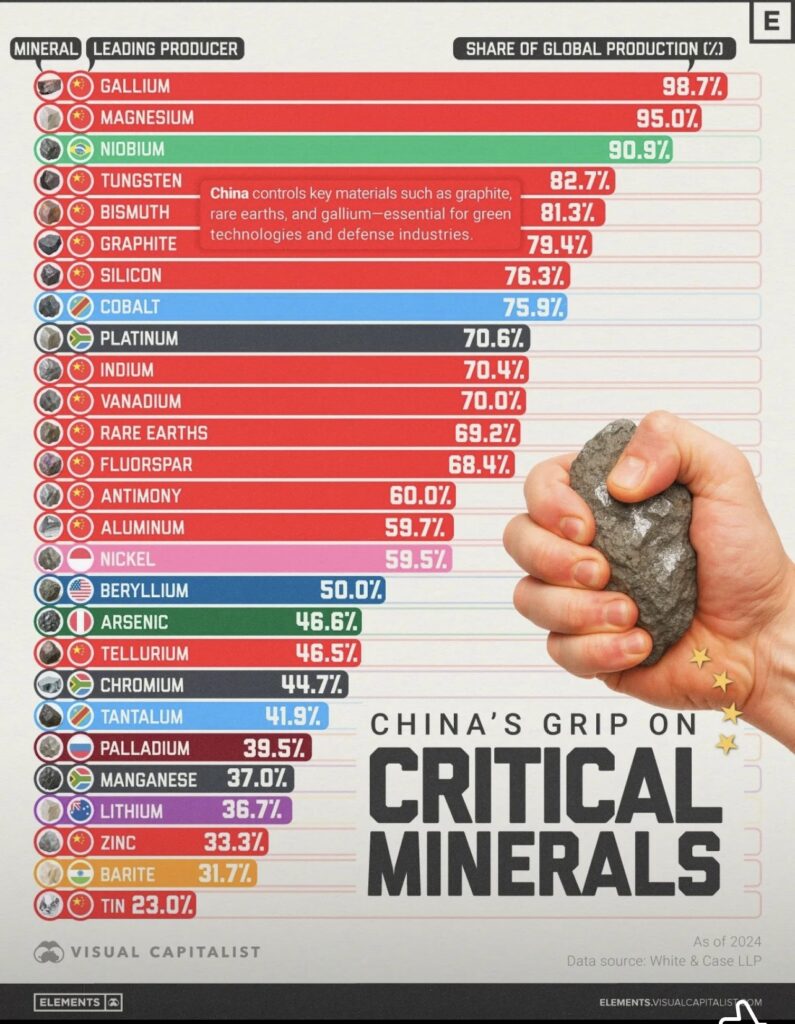

According to international analyses, China currently maintains a dominant position in most critical mineral supply chains. Many experts describe this as a form of “resource power concentration,” as the country controls the majority of global reserves and refining capacity for essential materials like gallium, magnesium, and tungsten. These are irreplaceable resources in the production of semiconductors, lightweight alloys, and advanced technological equipment. In the global renewable energy value chain—from solar panels to wind turbine rotors—China holds advantages spanning raw mineral supply, material extraction, refining technologies, and manufacturing infrastructure.

Industrial economist Professor Zhang Wei of Tsinghua University notes that long-term investments since the 1990s, combined with low labor costs and mastery of refining technologies, have enabled China to build formidable trade barriers. As a result, many countries that possess raw mineral deposits struggle with processing capacity and are forced to rely on Chinese expertise, creating a structural dependency that increases geopolitical risk.

In addition, for materials such as rare earth elements and graphite, China does not only possess a substantial share of global reserves; it also dominates refining capabilities, which is the most technically complex and highest-value segment of the chain. Renewable energy specialists argue that even if the United States and Europe accelerate investments in refining facilities, it will take years to diminish this dependence, as rare earth processing requires deep chemical expertise and decades of industrial experience.

While China holds the mineral power center of Asia, Brazil stands out as the only major supplier outside the region, controlling the vast majority of global niobium production. With one country holding a near-monopoly over a critical alloy component, Brazil occupies a strategic position in aerospace engineering, infrastructure construction, and industrial energy systems. Mineral trade expert Lucas Ribeiro states that Brazil’s importance will continue rising as demand for super-durable alloys expands alongside accelerating urbanization and the commercialization of aerospace technologies.

Meanwhile, the Democratic Republic of the Congo remains a key player in the cobalt and platinum supply chain. Cobalt is vital to electric vehicle batteries and energy storage, but mining operations in Congo face issues of human rights, conflict of interest, and political instability. Analysts warn that if nations continue relying on Congolese cobalt without pursuing alternatives—such as recycling or diversified sourcing—global supply chains may face disruption. Energy economist Terry Hall of London calls Congo a quintessential example of the “resource curse,” where a country rich in natural deposits but lacking domestic processing capacity sees most profits concentrated in foreign corporations.

As the global landscape shifts, Southeast Asia is emerging as a new center for refining and industrial support. The region benefits from sizable mineral reserves, an expanding manufacturing infrastructure, and government policies encouraging value-added production. Indonesia stands as a notable example after implementing a bold ban on raw nickel exports, compelling multinational corporations to build refining and battery facilities within the country. According to research published by the Bandung Institute of Technology, this policy has shifted economic value from simple extraction toward high-tech metal manufacturing, creating tens of thousands of jobs while increasing Indonesia’s bargaining power in global trade.

Meanwhile, Bangkok, Kuala Lumpur, Jakarta, and Ho Chi Minh City are becoming preferred destinations for foreign direct investment in battery technology, semiconductor materials, and metal recycling. This shift coincides with efforts by the United States, Japan, and Europe to diversify supply chains in response to geopolitical concerns. Economist Thomas Mayer observes that Southeast Asia is capitalizing on a strategic gap created by global “China +1” manufacturing policies, providing an alternative production base outside of Chinese territory.

However, the rapid rise of Southeast Asia in refining capabilities also presents new challenges. Environmental researchers caution that metal refining produces complicated chemical waste, requiring heavy investment in waste processing and regulatory frameworks. If nations prioritize short-term economic gains at the expense of environmental standards, they risk compromising long-term development. Singaporean environmental researcher Tan Qian argues that Southeast Asia must elevate its environmental regulations to meet European and Japanese standards, avoiding the “dirty industrialization trap.”

Policymakers increasingly recognize that the greatest value of mineral supply chains lies not in extraction but in refining technology, advanced material research, and industrial innovation. Raw exports enable foreign conglomerates to capture most of the profit margin. The current trend shows Southeast Asian governments investing in strategic material research centers, industrial support clusters, and comprehensive production ecosystems. Nations such as Indonesia, Malaysia, and Vietnam are deploying tax incentives, technological subsidies, and engineering training programs to support deeper industrial integration.

In a complex geopolitical context, many economists believe that the global mineral supply chain will no longer revolve around a single center. India, Australia, and Canada are investing heavily in rare earth mining and refining, while Europe increases metal recycling capacity to reduce reliance on new extraction. Yet Professor Stuart Hill notes that this transition will take years, providing Southeast Asia valuable time to climb the value ladder.

For Vietnam, the opportunity lies in deep integration into nickel, rare earth, and metal recycling supply chains. The country possesses the world’s second-largest rare earth reserves, much of which remains underutilized. If Vietnam develops refining technology and forms strategic international partnerships, it could become the region’s center for green industrial materials. Investment analyst Mark Reeves states that Vietnam benefits from a skilled workforce and geopolitically neutral position, attracting corporations seeking safety outside China.

In the coming decade, the most valuable elements of the mineral industry will revolve around material innovation, refining optimization, and high-tech product development. As transportation electrification accelerates, demand for nickel, cobalt, and lithium will continue increasing. Competition in this field is not solely economic—control over minerals translates into technological power. For this reason, analysts describe today’s mineral race as the “silicon battle” of the 21st century.

The world is witnessing a clear geographic shift in mineral value chains from the West toward Asia. China maintains dominance, Brazil consolidates unique advantages, Congo supplies essential materials, and Southeast Asia emerges as a global refining hub. Confronted with this competition, nations must invest in research, deep processing, and green technologies. Those who control future materials will command economic and technological influence in the new era.

Source: Collected from the internet

Related Posts

U.S. President Donald Trump’s Strategic Aluminum Tariff Reduction Policy: A Strategic Opportunity and Key Signal for Vietnam’s Aluminum Industry

U.S. Shifts Aluminum Strategy: What Does It Mean for Vietnam and the Global Market?

Vietnam Prepares to Produce Aluminum Ingots at the Dak Nong Aluminum Electrolysis Plant: A Milestone in Completing the Bauxite–Alumina–Aluminum Value Chain and Opening a New Era of Downstream Processing

Global Non-Ferrous Metals Market Enters the Summer Season: Five Key Trends Vietnamese Recycling Businesses Should Watch

A quick market update for VMRF members: Non-ferrous metals cool after a strong rally

Circular Economy: A Cornerstone of the European Union’s Sustainable Growth and Competitiveness Strategy